Payment of license

Internet payment is the foundation of Internet finance. Payment is a natural traffic entrance. It can be attacked and retreated. You can enter other financial services such as financial insurance lending, or cross-border cooperation; you can also take a step back as a payment tool, free of payment for other payment channels, and you can collect data yourself as part of future credit reporting.

Third-party payment starts traffic

The efforts of Alipay and Tenpay have changed the original payment habits of many consumers. Both online and offline can say that Alipay and Tenpay almost monopolize the entire consumer payment market. This year, WeChat Payment and Alipay have successively introduced the charging scheme. On the one hand, after the users are used to develop, the cost of their own payment service is reduced. On the other hand, by setting the threshold for the outflow of funds, the funds of individual users are kept as much as possible. In the system, or in its own consumption scenarios.

It can also be seen from this incident that the Chinese Internet payment market has transitioned from the “user training†stage to the “product innovation and service upgrade†stage. The Internet payment market relies on the product features itself, which will not change the user's landscape and market share too much. The next step is to compete for payment technology and payment services.

The "user training" period has passed, and everyone is thinking about how to make money. Whether it is self-contained Alipay, Tenpay and other independent third-party payment products such as Lakara, they are actively deploying consumer finance business, and other financial services are derived from payment. However, the current financial business is only in the scope of its own business, and few companies can achieve cross-border cooperation.

In the era of realizing traffic, payment companies are looking for new profit models and profitable areas such as diversification and internationalization with the core of payment functions. Payment is the only way for commercial realization, online consumption scenes are becoming more and more abundant, and the online payment market will continue to expand. With the Internet, the offline payment market began to optimize its business model. Therefore, by expanding the financial business to expand its business source online, offline can provide value-added services for B-end users and increase reconciliation, marketing, and risk control.

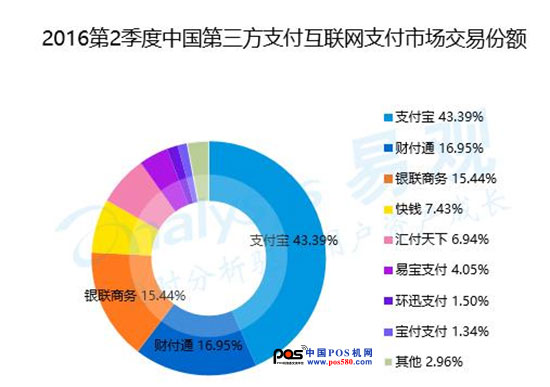

The dilemma of third party payment

The road to realizing third-party payment is not so smooth. Alipay and Tenpay have the absolute status of third-party payment, and have always occupied a stable market. It is difficult for other Internet companies to break through!

(Screenshot on Yi Guan think tank)

Therefore, it is difficult for other Internet payment companies to break through! ! !

However, it cannot be said that other payment companies have no chance at all. After all, the current market structure is relatively clear. Next, the entire Internet finance will be dominated by financial technology development, and model innovation is not the core competitiveness of most products. Therefore, in terms of payment technology, it is possible to go ahead of other payment companies and have traffic to break into the game. For example, the US group launched a smart pos machine in Wuzhen, which is a breakthrough, but the market recognition is high and unclear.

The vitality of the fourth party payment

After the war of third-party payment, it ushered in a vitality paid by the fourth party. Fourth party payment is an integrated payment platform that integrates third party payments. According to incomplete statistics, there were 8 fourth-party payment platforms that were financed in 2016. See the table below for details:

2016 China's fourth party payment product financing situation

The natural advantage of fourth-party payments is that they can meet the fragmentation needs of consumers. In the tide of mobile payment, the characteristics of the payment scene becoming more differentiated and fragmented determine that it is impossible to have a dominant market structure, and the diversified situation of hegemony will create a living space for the development of the fourth party.

The fourth party can close the distance between the merchant and the consumer. Through this weak relationship, if some daily maintenance work can be added, it may turn into a strong relationship, and then explore more consumer demand and consumption scenarios. . In addition to helping merchants connect with a large number of third-party payment products, fourth-party payment can also help merchants to view their financial situation and consumer records, and also help merchants achieve accurate marketing. This is one of the reasons why fourth-party payments are favored by the capital market this year.

Alipay internationalization has just begun

On November 22, 2016, Korea New World Group and Alipay reached a strategic strategic cooperation. In fact, Alipay has already entered the payment market in South Korea. In the past two years in the streets of South Korea, more and more merchants have the function of “Alipay Paymentâ€. Alipay has become an emerging payment method for Korean Chinese tourists gathering areas, from tax rebates, to shopping, to transportation (Alipay T-money card), Alipay can be all done.

South Korea is only the starting point for Alipay to enter the international market. South Korea can attract a large number of Chinese tourists every year, so it is piloted by South Korea. Although the test of water in South Korea is successful, the internationalization of Alipay may not be good. Consumers in developed countries like to use credit cards. The payment equipment and conditions in developing countries are relatively backward. Alipay wants to be international. It’s easy, but the path to internationalization is inevitable.

Expected payment technology

On April Fool's Day 2014, Alipay proposed the concept of “empty paymentâ€. By scanning the authorization and setting the limit, you can give any physical value and pay with the physical object.

Around June of this year, Visa Europe proposed a new e-commerce solution that uses AR technology to achieve online shopping and online payment.

And Apple, Xiaomi, Samsung and other companies have launched NFC payment (near-field payment, new mobile payment methods that can be paid through terminal devices such as mobile phones).

Artificial intelligence, cloud computing and other technical means will lead the payment market to become intelligent, and also bring more imagination to the future payment market. This is also an opportunity for other payment companies, which has cast a veil on the future payment market.

Interactive conference teaching touch all-in-one machine, integrating Windows and Android dual systems, injecting AI elements, focusing on multiple human interactions, display, movement, and interaction usher in a new smart classroom and smart conference, widely used in multimedia teaching And meeting scenes.

Our factory has a professional interactive whiteboard R&D team, has Conference Interactive Whiteboard, Teaching Interactive Whiteboard, conference all-in-one machine and interactive smart board full production line of products, and the products sell well at home and abroad.

Conference Interactive Whiteboard,Teaching Interactive Whiteboard,Conference All-In-One Machine,Interactive Smart Board

Guangdong Zecheng Intelligent Technology Co., Ltd , https://www.szzcsecurity.com